How To Find Free Money

How To Find Free Money

Getting serious about your debt

Hello Travelers. I am re-posting this article from my website in case some of you have not had opportunity to read it.

In part one of the article "How to Get Control of Your Debt" series, we're going to talk about finding free money and touch a bit on budgeting.

Let's get started:

How Can You Find Free Money?

This is not some get rich-quick scheme and it won't be some weird thing you'll have to ponder over to figure it out. It will take work, planning and your undivided attention.

Raise your hand if you eat out for lunch at work everyday.

Raise your hand if you stop off at Starbuck's or your local bakery for coffee and danish every morning before work?

Raise your hand if you're renting the modem and wifi equipment from your cable company.

Raise your hand if you spend lots of money on little "incidentals" each week.

If you can raise your hand to even one of these, then you've just found your FREE MONEY.

It is so easy for us to fall into routines or to say "it's easier if..." instead of stopping, thinking and planning our finances. My Dad had a saying: "I have more time than money, so I spend the majority of my time watching my money."

Growing up and hearing my Dad say this, I never understood. But now that I have a teenager, a mortgage and a few credit cards, I completely get it.

Everyone on planet Earth is under the influence of Uranus in Taurus. And in the natural horoscope Taurus rules the 2nd house.

The 2nd house of the natural zodiac rules: money, security , safety, possessions and questions of self-worth.

In personal terms, the 2nd house rules all that you own/earn/owe; stocks and bonds, rent, mortgages, car payments, etc. The 2nd house is the house of safety and security - do you have a comfortable safe place to live, in a decent neighborhood? Do you have enough good food and drink to sustain you? Can you afford things like a decent car, nice clothes, a vacation or an entertainment center?

These are the practical, third dimension things that come with the 2nd house.

In the natural zodiac, the 2nd house is ruled by the sign Taurus and Taurus rules: property, currency (so banks), commodities (the stock market), agriculture (weather and prices) and yes, cows (which were a form of currency back in the olden days).

Uranus is the planet responsible for shocks, upsets, rapid cycles of up & down. He rules electricity - so think of waves or cycles of electricity running to-and-fro through a wire - if it's not contained -why it can suddenly explode! Uranus is the God of the Sky and he's responsible for freak storms, lightening storms and unexpected freak weather that catches you off guard.

Now, think about this huge planet of Air and Electricity sitting in the Sign of Earth and stability....well, you might be able to see the conditions and possibilities and how global markets can be affected.

I started this article about 4 days ago and yesterday, 26 September, the bottom fell out of the US stock market and the British Pound fell to its lowest level since 1971.

I feel that things will only get "tighter" as we begin to move into the winter months. Already here in the US, gasoline prices are starting to rise again - just in time for the holiday season and start of cold weather.

Getting back to the 2nd house - with Uranus here - it means ups and down in the stock markets, with currency, food prices, property prices and this in turn affects you in your wallet. When all the essentials that you need are rising in price and you've only a set amount of money each month, then you're gonna need a plan:

Sit down and write out how much money you earn (from both regular work and side hustles).

Next, write out all your monthly expenses.

Write out all your credit card amounts, loans, car payments, etc.

Write out all your subscriptions - Amazon, Prime Video, Netflix, Google, Apple, Roku, etc.

Write out - on average how many times a week you: buy coffee at Starbucks, for example; eat out, go to the pub, etc.

Write out how much you spend at the grocer's.

Write out how much you spend on personal hygiene items.

This is a LOT of work, but the idea is to discover where your money is GOING. Doing this you can find out where you might be able to cut back on things and save money.

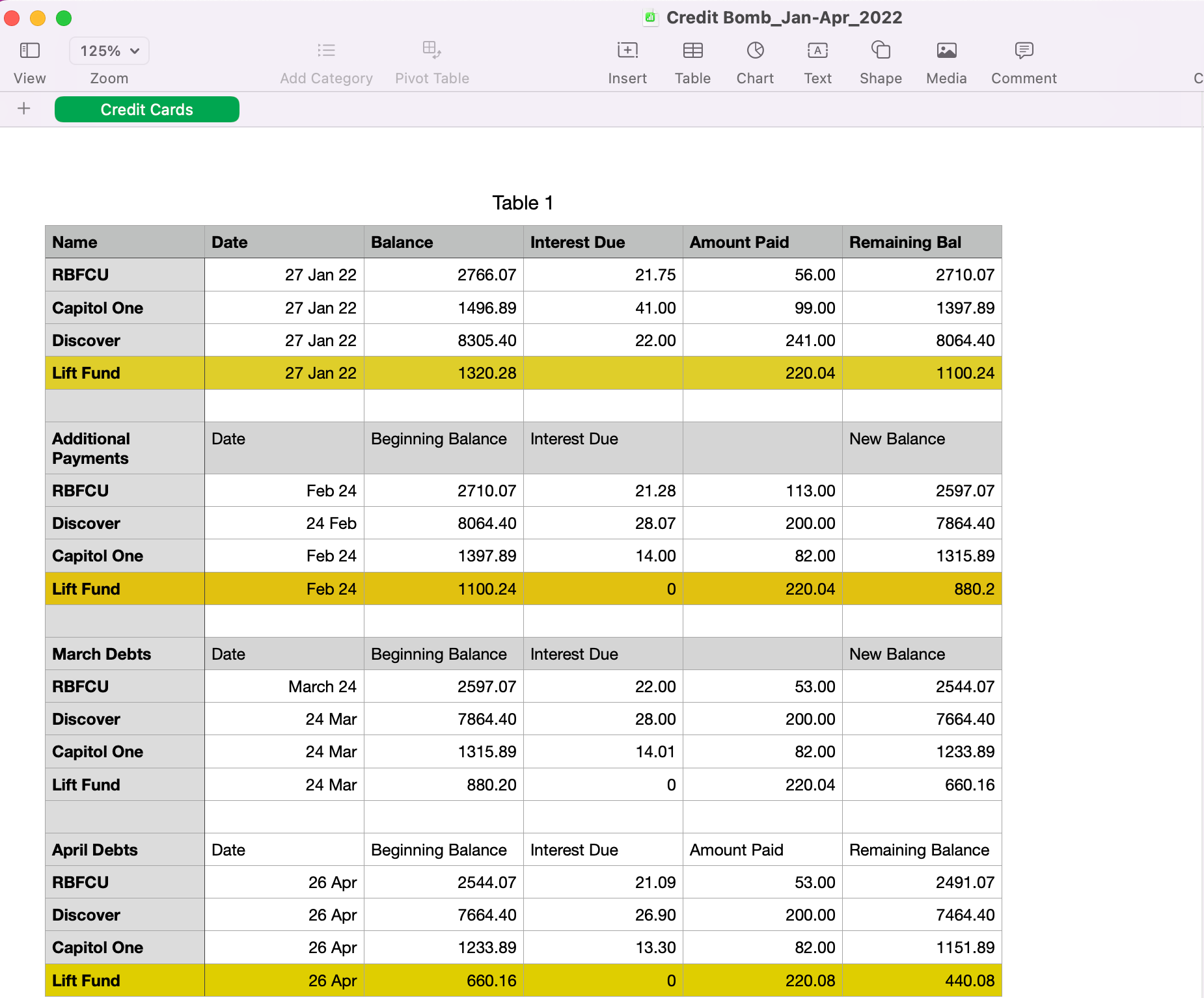

Once you have all your numbers, you can then create yourself a spread sheet using Microsoft Excel, Google Docs, Apple Numbers or you can just get a notebook. Here's an example of a Credit Snowball sheet I made at the start of 2022:

2022 Credit Snowball Sheet

The item listed in yellow, was a business loan I took out for new equipment under the Pandemic Business Act. It had zero interest and was the 2nd to the smallest debt I had....but because it had zero interest I was able to take what money that would've been added for interest and move it over to my SMALLEST debt which was Capitol One.

Monthly payment for Capitol One was $41/mo. One month I paid $99 then I made $82 each month and in four months was able to reduce the debt down by $325. While this doesn't sound like much, just being able to see that I was able to do that by paying more than the minimum payment, was a great feeling. And as you lower the amount owed - YOUR INTEREST RATE GOES DOWN TOO.

If I'd just stuck to the minimum $41/mo - I would not have made a dent in in the amount owed as the interest rate each month would just add up. And you should keep in mind that interest rates fluctuate everyday. I don't know of too many credit card companies that offer fixed rates, but if you have one - count yourself lucky. Here in America, interest rates can be as high as 28%.

The longer you carry the debt, the more money you'll end up paying to the company, so it behooves you to pay as much as you can each month - without fail.

The Lift Fund was paid off in 5 months - a $220.04 payment in May and the last one was June.

Now, since that time, a few of my cards have increased in debt - I used a few of the cards, but more importantly - I fell off the wagon and stopped keeping up with my budgets, writing out everything I spent and credit bombing. And truth- my finances are the poorer for it.

But if you'll write out all your expenses and keep track of it; and if you'll make yourself a Credit Bomb worksheet and STICK TO IT, you'll find yourself getting out of debt faster than you realize.

All those store bought coffees, eating out, subscriptions that you could probably do without, etc - by keeping track of where the money goes, you can find places where you can eliminate some things and then with the money saved, you can either apply it to your debts or add it to your emergency fund. You could even do both!

Lastly, find a budget app that you can download to your phone. This way, if you're out and about and spend money on something, you can immediately deduct that amount from your budget.

I use Fudget - budget app over on iOS and have it installed on both my handheld and MacBook. But there are hundreds of budget apps for your phone, so find the one that works best for you. Then USE IT.

Tip: Once a year, you can get a free credit report from each of the credit rating agencies (Transunion, Equifax and Experian). You can do this by going online to each of their sites and find the “request report” or you can write them.

Tip: Did you know that once a year, you can call your credit card company and see if they are willing to give you a lower interest rate?

Tip: Some credit card companies will give you an automatic raise in credit limit amount. But you don't HAVE TO ACCEPT IT. While it may boost your credit score, it'll also tempt you to spend more, so be careful with this one.

Tip: If you don't have a bank account, then get some plain white envelops and write on each one what money goes into it, for instance: Groceries, Electric Bill, Gas, Rent, Personal Hygiene, etc. Then write your budgeted amount on the outside. When you get paid, put that amount in your envelope and use that money ONLY FOR WHAT IT IS MARKED FOR.

Tip: Did you know you can call your cable company to see if they have any specials or deals and ask if they are willing to sign you up for them?

Negotiate. This is a skill that most of us do not possess when it comes to our finances. We simply accept that something is the price we're told and never think to ask if there's a better price. Ask. The worst thing they can say is "No, that's the price." But if you don't ask, you may miss an opportunity to save a bit of money.

Like I said - it's lots of work and hard work. But keeping in mind what my Dad said: "I have more time than money, so I spend all my time watching my money" - means watch your spending, be aware of what you're spending on and keep track of where your dollars go. This brings another benefit - it makes you stop and think about buying things or spending money on something that may add no real value to your life.

That's the 2nd house in a nutshell - who or what is more important than money or gold? It's about value and value systems, safety, security and all that you own, earn or owe.

And wouldn't you rather earn and own, than owe? I know I would.

In part 2 of this article, we’ll take a look at mortgages.

Until then.

Be Good To Yourselves.

Hello Tara,

I want to thank you for this great article which has come at a momentous time in my life. I do need more clarity about my money, and in these unprecedented times, I need to watch where I spend my money and why. This is helping me get a good start on having the freedom I want, which money can give you if you work with it properly. Have a great day!

Tara, I found you recent article on finance to be informative. Many of us know little or nothing about financial literacy. Your article is a good read. ,